- Why “big”? Because you’ve probably only been getting half the story, and more minutia than you need.

- Why picture? Because the Starpoints-Marriott Merger, coming into effect on August 1, reframes the landscape.

- Why be happy? FCF’s new Credit Card-iogram widget makes you an Einstein.

My mom used to say, be careful about believing in what you read in the papers. In 2018, that applies in spades to the Internet, and in particular, credit card recommendations made on the Internet. I say this because I think the discussion is biased toward the earning rather than the spending benefits of cards.

You’re only getting half the story. The truth is, what some cards lack in earning advantages, they more than make up in spending opportunities.

[aside headline="NO! WE’RE NOT TALKING TO YOU:" alignment="alignright" width="big" headline_size="default"]

Coupon Clippers, who’ll spend an hour to save $10.

Point Pinchers, who have ten cards to cover every spend category bonus, not to mention the time spent to track everything. As a beloved FCF staffer said: “I couldn’t think of anything worse!”

Bank-Currency Bounders, which are locked in to bank currencies like Capital One. It’s a no-go for premium travelers, as these cards are largely focused on coach travel.

Cash-Back Seekers: Also, a big mistake for the premium traveler.

Balance Carriers: Big, mistake. Pay off your cards monthly or get slammed with interest payments.

Credit Card Churners, who get credit cards only for the sign-up bonus and then cancel afterwards.

Capped Crusaders, who get cards that have a low bonus cap, such as the American Express Everyday Preferred Card, which has a $6,000 cap on supermarket bonuses. Getting an extra 18,000 miles or so a year through this card isn’t worth it.

Those Living Outside the U.S: You have similar opportunities, but the cards and partnerships are very different, so use this as a conceptual guide./aside]

It’s exacerbated by the fact that most online commentators are getting huge kickbacks for recommending every card that surfaces—because the payout for these commentators is up to $300 for every card you sign up for through their links. How many realize this?

No wonder they’re telling you to have an “awesome foursome” of cards, because that’s more money in their pocket: $1,200 worth to them—the so-called “free” websites.

There’s more to say about this group, and the true “cost of free,” but first let’s lay the cards on the table.

The Starwood-Marriott Merger

As most of you know, the Starwood Amex has been our favorite card for a long time. It meant users could be as lazy as they wanted to be, knowing that this card was a no-brainer, especially for everyday, non-bonused spending—the largest category for many.

Given the impending, August 1, changes, what now? Is there a new favorite? We’ve got answers, not to mention a cool widget we’re calling FCF’s Credit Card-iogram, to help get your potential fortune told.

THE TRUTH IS, THERE IS NO CLEAR WINNER

We don’t have a clear-cut new favorite card to replace the Starwood Amex—for The Lazy Upgrader. So now you need to do a little extra thinking (don’t worry, we’ve been doing the cramming and reduced to an FCF Top 10 list). It works because it is tailored to your spending—and redeeming—habits.

CREDIT CARDS ARE A TWO-WAY STREET: EARNING and SPENDING

Many people think of credit cards in terms of the points they earn. “Wow: 3X [miles/points per dollar spent]! Must be better than 2X, right?” Not necessarily. You should be thinking about what you’re using your credit card points/miles for, the redemptions they offer, and the amazing Business and First Class deals they can unlock—or not unlock.

Let’s break that down a little. You might earn double (2X) the points per dollar spent, but the cost to redeem might also be double. So, they cancel each other out, or as they say, it’s a wash.

Or worse, you might earn 2X points for some spending, however, the cost to redeem an airline award is three times (3X) the amount. So, you lose out.

Help is at Hand, Literally

Our new Credit Card-iogram Widget can help. It’s a comparison of credit cards (curated by us, so they’re the cream of the credit crop, as determined by the FCF Upgrade Mindset) based on Earning Opportunities and Spending Opportunities. Version 1 has just been released.

When you earn points, it’s not game-over, it’s game-begin. In the same way that stocks are worthless until you sell them, your points are too—worthless until used. So, you may as well maximize their value.

My equation for the best card is simply this:

Best Credit Card

=

Spending Opportunities

Xs

Earning Opportunities

[aside headline="DEVALUED BUT STILL WORTH MORE" alignment="aligncenter" width="big" headline_size="default"]

Our longtime favorite Starwood Amex is being devalued as a result of the Marriott merger in terms of the points it earns (from 1.25 miles per dollar to .825—a 34% drop), and that sounds like a passion killer.

But its ever so lucrative currency remains. And by that I mean connection and flexibility. It will link to more than 50 airlines come August 1.

That gives you access to some of the world’s best airline deals. We call multi-currency cards like these “Elastic Plastic” because they stretch your opportunity. In other words, there will be some that will want to keep and still use their Amex SPG credit card.[/aside]

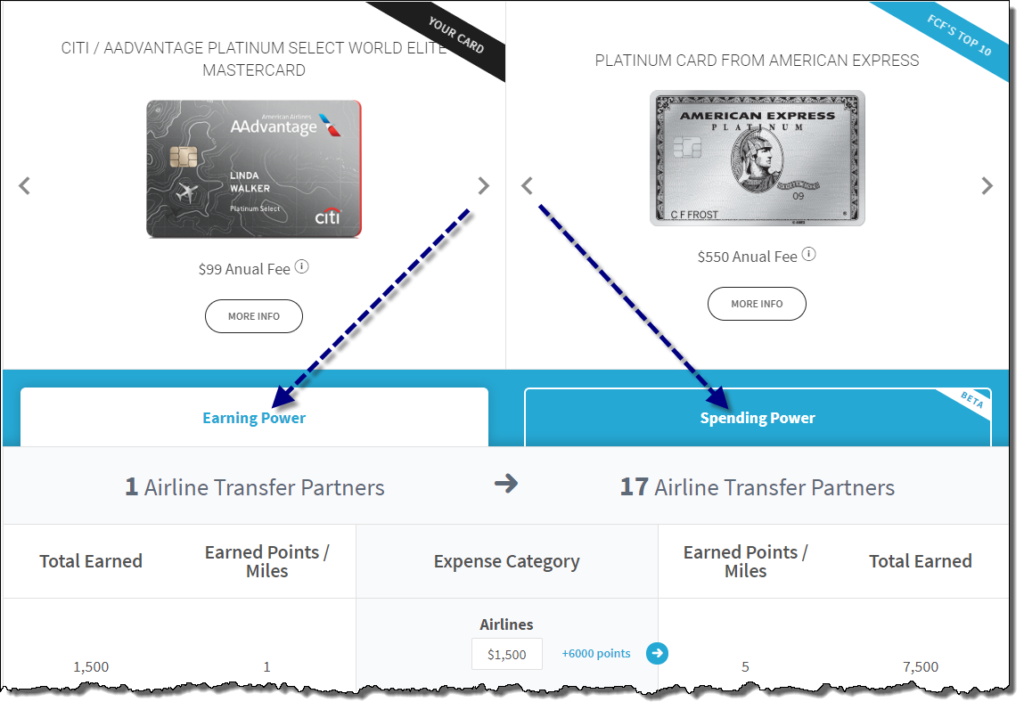

THE FCF CREDIT CARD-IOGRAM

Simply choose your card on the left, and one of FCF’s curated favorites on the right. Then compare them by Earning Power and Spending Power—and by FCF’s Favorite Upgrade Strategies.

Example Super-Power Spending #1. FCF’s Leg Stretch Strategy nets four long-haul segments in Business Class on American flights for 100,000 miles when using Japan Airlines (JAL) miles.

To get the advantages of JAL miles going forward without the Starwood Amex, look at the Barclay’s Arrival Premier World Elite Mastercard. It earns ~1.17 miles per-dollar-spent for everyday spending. It’s something to consider instead the Chase cards, if you’re not so impressed by the spending power of the bank’s Ultimate Rewards points currency, even though you can get 3 points per dollar spent for several spend categories.

If you’re anything like me, you go after low-hanging, high-return Chase points for a while then seek to quick diversify into points with much greater spending power.

For the purpose of diversification, if only because of the need for as many options as possible due to the difficulty of finding available miles seats at saver rates, if not many other reasons.

Example Super-Power Spending #2. FCF’s Ultimate Mileage Award Ticket with All Nippon nets an Around-the-World Business Class ticket starting at 105,000 miles. Incredible!

To get All Nippon miles, look at any of the American Express cards included. One of the highest earning cards is the American Express Platinum card. It offers five points (5X) per dollar on flights booked on airline websites (other purchases are 1 point). Amex has 20 airline partners and is the second-strongest currency, behind Starwood/Marriott, from The Lazy Upgrader’s perspective.

Consider this instead of earning miles with other cards that offer more points for various other categories, which may in the end charge you double or triple when you go to redeem—and with only a few great transfer partners.

You have to look at your options based on what you want to use your points for.

THINK BIG, NOT SMALL

Curious to see what Google and her friends had to say on this topic, I found search after search resulting in commentators—or bank-card shills—talking about the Return-on-Credit-Card-Spend (RoCCS) in terms of, “I saved 1.7% … 2.0% … 4.5%!”

Meh.

Don’t sweat the small stuff. Life’s too short, and your time too valuable to be quibbling over one percent of not a lot. If you’re happy to delve into that kind of minutiae, then this piece is NOT for you.

Let’s do the math.

Say you spend $2,000 a month on your credit card. A 2% discount means you’ll save $480 a year. But you can get a cash-back card with zero effort for no annual fee. So, for every $2,000 you spend on your card each month, in effect, you’re making $480 a year. Those are bad numbers for smart FCFers.

Gas is a good example. Some folks put a premium on getting the right credit card for gas-station visits. (Can you believe it?) But what’s the difference between 1X and 2X points on a small overall expense like that? I’m spending around $300 a month on gas (yeah, I drive a guzzler). So, if I use a 1X card instead of 2X, I miss out on 3,600 points annually.

But hold on—I can buy those points for just $90 with Amex Rewards or elsewhere. Buy double or triple the gas I do? So what? Just multiply by $90. Why spend the mental energy remembering to use a card in my pocket every now and then, and then keeping track of it, all for $90? Reminds me of that sweet meme: Ain’t nobody got time for that!

HOW MANY MILES WILL YOU GET OUT OF BED FOR?

Maybe it’s because I’ve been running FCF for 21 years that small numbers just don’t do it for me. What gets my attention is a 40% or 50% discount. For example, getting a $30,000 First Class ticket at 90% off. Or staying at the Ritz Carlton in New York for free for a seven-night stay, worth $5,600. Or a Round-the-World award for less then what Delta charges for a ticket to Europe.

That’s what fluffs my pillow

Speaking of maximizing your money, it’s also good to know that upgrading to premium air travel nets a far higher return-on-miles than any other redemption option. For example, a typical return-on-miles for economy class travel is generally 1¢ to 2¢, whereas premium air travel can easily net 5¢ to 10¢—or even more if you choose the right route or airline.

What we at FCF call “The Upgrade Mindset” is all about value. It’s comprised of relatively straightforward elements and one of them is reducing complexity.

“Lazy upgrading” is one way to put it, but it’s actually smart upgrading because you’re not wasting mental energy on low-value calls. The Upgrade Mindset looks at the big picture. As with an FCF subscription, you can make up the cost with just one sweet redeem.

HOW ANYONE CAN GET A BUSINESS CREDIT CARD

More than a third of FCF’s members are business owners, so it’s not hard to get one of these cards. For non-business owners, in California for example, registering a sole proprietorship is inexpensive and can be done quickly online. It’s my understanding that in most states the rules are similar to California’s—so depending on your spending levels, it takes almost no effort to qualify for the business cards in our top 10, in particular, Chase Ink Business Preferred.

TRUE LOVE DOESN’T MEAN YOU HAVE TO SHARE CARDS

Many cards have bonus limits. While the Chase Ink Business Preferred card gives you 3X points per dollar on travel, it’s capped at $150,000 annually. If you and your spouse have separate cards, however, you have double the bonus opportunity. The same goes with sign-up bonuses. Never “add” someone to your account—have them get their own card so you can reap the bonus twice.

[aside headline="Who’s Paying Whom, Again? " alignment="aligncenter" width="big" headline_size="default"]

As mentioned above, before you adopt the thinking advocated on a “free” travel site, count the cost. Commissions rule. It’s no surprise when these folks recommend that you have a wallet full of cards when they get nice kickbacks on them—up to $300 each!

FCF doesn’t taint its editorial this way nor encodes links in our text that nets us phat checks in the mail off of your back.

[/aside]

FCF’s Play Your Cards Right Cribsheet

[table_opt id="5971" style="gray-header" width="default" alignment="thcenter" heading="thcenter" rows="tdcenter" responsive="no" /]

Elastic Plastic Partner Cheat Sheet

[table_opt id="5970" style="gray-header" width="default" alignment="thcenter" heading="thcenter" rows="tdcenter" responsive="no" /]

- Why “big”? Because you’ve probably only been getting half the story, and more minutia than you need.

- Why picture? Because the Starpoints-Marriott Merger, coming into effect on August 1, reframes the landscape.

- Why be happy? FCF’s new Credit Card-iogram widget makes you an Einstein.

My mom used to say, be careful about believing in what you read in the papers. In 2018, that applies in spades to the Internet, and in particular, credit card recommendations made on the Internet. I say this because I think the discussion is biased toward the earning rather than the spending benefits of cards.

You’re only getting half the story. The truth is, what some cards lack in earning advantages, they more than make up in spending opportunities.

[aside headline="NO! WE’RE NOT TALKING TO YOU:" alignment="alignright" width="big" headline_size="default"]

Coupon Clippers, who’ll spend an hour to save $10.

Point Pinchers, who have ten cards to cover every spend category bonus, not to mention the time spent to track everything. As a beloved FCF staffer said: “I couldn’t think of anything worse!”

Bank-Currency Bounders, which are locked in to bank currencies like Capital One. It’s a no-go for premium travelers, as...